Across the world, billions of citizens in dozens of different countries have no access to the financial tools many of us take for granted each day. Products like savings accounts that earn interest on deposits and allow people to build wealth over time are a crucial part of advanced economies that help citizens escape poverty. Access to loans, even in small amounts of just a few hundred dollars, can mean the difference between keeping a small business alive or being forced back into subsistence living.

The people who lack access to these basic financial services are commonly known as the ‘unbanked’. According to data from the World Bank, more than 98 percent of citizens over 15 in countries like Canada, Norway, and Japan at a minimum have a bank account offering access to basic services. It might come as a surprise, though, that nearly 7 percent of the population of the United States over 15 don’t have a bank account, and lack access to basic saving and borrowing products. In other parts of the world, just 70 percent of Brasilians and less than 50 percent of Indonesians have bank accounts. And in countries like Iraq, Cambodia, and Pakistan, less than a quarter of the adult population have access to basic financial tools.

Cryptocurrency has the potential to give billions of unbanked citizens around the world access to the financial resources they need. By using decentralized applications built on protocols like Tendermint, unbanked citizens can gain access to highly secure, individualized accounts (or ‘wallets’) to save funds, less expensive remittance payments, and the ability to store value in ‘stablecoins’ -- assets pegged to different national currencies to better defend against volatility and inflation. Free, reliable access to these tools can make an incredible impact on the quality of life for billions of unbanked people around the world.

When Your Wallet Is Your Bank

Getting started with cryptocurrency usually means getting set up with a place to store, receive, and send digital assets, commonly referred to as a wallet. Crypto wallets are effectively impossible to hack and can’t be deleted or erased. Each wallet, like each bank account, is unique, providing an electronic address friends or businesses can use to identify the owner and send or request money. More advanced wallets and other decentralized applications allow users to deposit money and earn interest, but we’ll stick to the basics for now.

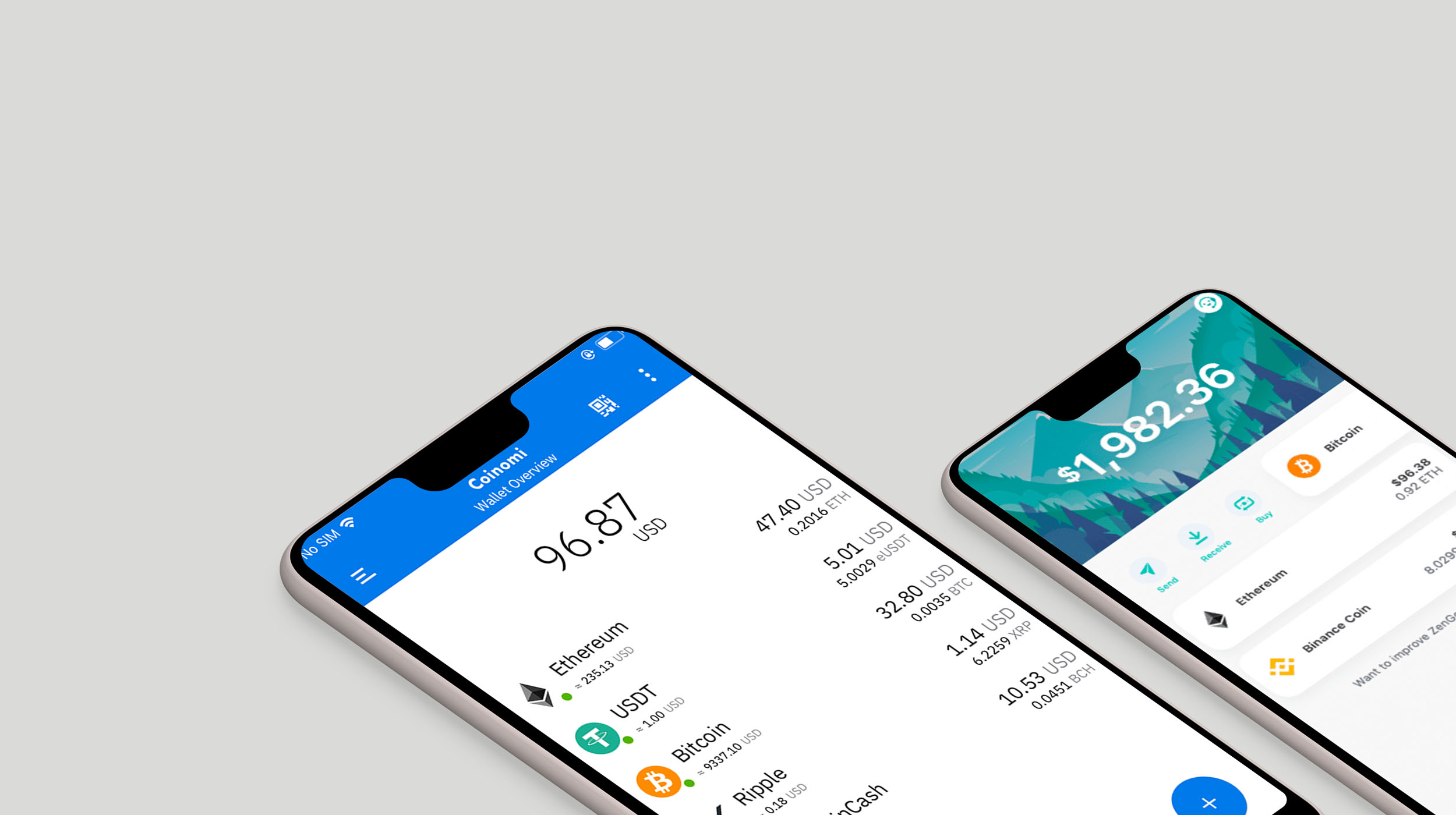

ZenGo is a popular wallet that can be used from a mobile device. ZenGo wallets are free for the time being and offer in-app support and help back up passwords you’ll need to access your funds. ZenGo wallets even allow users to buy cryptocurrencies directly from their phones and opt in to programs that earn some interest on saved money. Since ZenGo offers several services that go beyond basic wallet functionality, eventually they expect to begin charging a small monthly fee to use. For now though, ZenGo is completely free and one of the best ways for unbanked people to start getting familiar with crypto with some added guide rails for extra security.

For those who already have some crypto experience, a Coinomi wallet will always be free and offers all the standard functionality of a good crypto wallet. For those prioritizing security, investing in a separate physical device to store your crypto is a good option - a Ledger Nano S can be had for about $60 USD.

After setting up a crypto wallet, it’s time to start receiving payments! One of the most common ways for unbanked citizens to meet their daily needs comes from remittance payments, or payments sent from friends or family working in other countries.

Crypto Remittance

According to the World Bank, the cost of sending a $200 USD remittance is 7 percent of the total on average across the globe. In many cases, these payments are received at a post office or bank branch (even if the recipient has no account), often taking days to complete a transfer and in many cases requiring long trips to urban areas for unbanked citizens in rural communities. Crypto offers a better way.

One of the most appealing aspects of cryptocurrency transactions in general are very low fees. Hundreds or thousands of dollars can typically be sent between cryptocurrency wallets for just a few dozen cents. Instead of paying for corporate salaries or other operating costs of centralized money transfer services, the fees paid to transfer crypto go directly to the people running the computers that power decentralized crypto networks.

Bitcoin and Ethereum, the two most popular cryptocurrencies, are good choices for the first steps in sending remittance via crypto. Instead of heading to a bank or Western Union, the sender buys crypto using an ‘on-ramp’, or a service that buys and sells crypto in exchange for USD or other national currencies. Coinbase is the most popular service for moving between crypt and fiat currencies like dollars, and provides service in more than 30 countries around the world. After that, all that’s required is the wallet address of the recipient for the sender to transmit the payment. Depending on the cryptocurrency used, the transaction can take from a few seconds up to about 30 minutes. No banks, lower fees, and all performed online from the comfort of home or any place with internet access.

Spending Money

Receiving payments or holding savings in crypto is not much use if you can’t spend it eventually. More and more online merchants will accept common cryptocurrencies as a form of payment, but holding crypto for extended periods can also be risky. Unlike some national currencies, the value of Bitcoin or Ethereum can change dramatically over the course of a few weeks or even a few hours. If payments received in crypto are intended to be used for daily spending needs, recipients in many countries can use Coinbase or other local services to convert back into local fiat currencies. Decentralized local networks like LocalBitcoins are another option, where individuals offer to convert between crypto and fiat for a fee they set themselves.

On the other hand, payment recipients in many countries might not want to convert into local currency due to the risk of inflation or simply to retain the greater security of holding savings on their mobile device. However, it’s still important to protect against the changes in value common in most cryptocurrencies. In that case, ‘stablecoins’ offer all the benefits of digital currency while keeping a steady value, usually tied to the value of the US dollar. Using Bitcoin or Ethereum to buy $200 worth of USD Coin (USDC) or Tether USD (TUSD), two of the most popular stablecoins, means you can always sell those assets for $200, even if the crypto you used to buy them is worth just $100 a year from now. Crypto can be used to buy stablecoins through wallets like ZenGo or Coinomi, and can be sent electronically with low fees like any other crypto.

Lacking access to financial services like reliable savings accounts and stable currency makes life harder than it needs to be for more than a billion unbanked citizens around the world. By learning the basics of buying, holding, and using cryptocurrencies, 21st century technology has opened the door to financial inclusion for unbanked citizens ready to grab their piece of the cryptocurrency revolution.

ANATHA

Designed for Humans

Together, let’s create tangible solutions to systemic global problems.

Sign up for our newsletter, THE PRACTICAL IDEALIST, created for anyone who believes the system needs a major upgrade

We want to foster the future economy of generosity — structures which promote human flourishing, systems in which human needs come first. We not only believe that such systems are inevitable, we're helping make them a reality by returning real spendable value back to our community.

For newsletter, product updates, and more.