What’s most misleading about the word “wallet” is that it suggests that “money” flows out. We carry wallets in the world not to acquire money but to spend it as we make our way buying lattes, lunch, and gadgets. It’s very rare to have money flowing into your wallet as you go about your day. But crypto “wallets” should sit at the juncture of our very participation in the information economy, “money” flowing in and out continuously.

Whenever a new technology demands new modes of thinking, we generally resort to old metaphors. For example, we still talk about web pages, folders, and desktops—all these phrases from the now outdated office. While many of them are useful and help people understand the new by applying a known figure, these inherited words also limit our understanding of how new technologies can operate.

Is “Wallet” the Right Word for a Cryptocurrency Wallet?

Today, the cryptocurrency world talks about “wallets.” It’s not a terrible word, for sure, and it’s not totally wrong. A crypto wallet, like a real world wallet, seemingly holds your “money” to store and spend (even if, technically, it doesn’t hold your tokens but rather holds your keys — so, to be precise, it’s a keychain — but that’s confusing to most people). And yet we’re already pushing against the limits of that word, “wallet.” After all, are all cryptocurrency tokens in fact money?

But what’s most misleading about the word “wallet” is that it suggests that “money” flows out. We carry wallets in the world not to acquire money but to spend it as we make our way buying lattes, lunch, and gadgets. It’s very rare to have money flowing into your wallet as you go about your day. Sure, you refill it from the ATM — but that’s not really money flowing in as it’s already your money. No, 99.99% of the time, money is flowing out of your wallet to businesses.

There are many different kinds of crypto wallets for different purposes and benefits — cold (hardware wallets), hot (software), light, and some that act like wallets but are just centralized storage (such as Coinbase) so the funds are not really yours (“not your keys, not your coins”).

In almost all these cases, wallets are standalone applications to store, manage, send, and receive cryptocurrencies. They’re as much “banks” as they are “wallets” as we use them not just to store and send tokens but to manage our portfolios and earn interest. They’re necessary, too, as we have to put our tokens somewhere.

But they’re limited, cut off from the more general flow of value. If you want to add new tokens, you usually have to get them from a crypto exchange, such as Kraken, and then send them to your wallet. Today’s crypto wallets are little islands — secure (hopefully!) and useful but, alas, less dramatically useful by being isolated from the actual creation and flow of value.

Frictionless Payments? More Like Frictionless Spending.

Recently, the fiat world has been working hard to place our fiat wallets directly in the flow of value — well, in the flow of expenditure. Today, virtual payment platforms like Apple Pay, Google Pay, and PayPal are increasingly integrated into the buying process. They try to make it seem like you’re not reaching for your wallet to buy something but are part of the very system itself. This makes spending money seamless and is touted as a great function making our lives easier.

But it’s hard not to notice that these services are created to expedite you spending money. Frictionless payments, they call it: now you’re free to buy to your heart’s content — or until your credit card is denied because you maxed it out buying crap, albeit friction-free.

Note how when it comes to our wallets and services, we never talk about frictionless acquisition — only frictionless spending. The use of the word “wallet,” alas, reinforces this thinking. This construction is meant to make you spend your money as easily and quickly as possible while conveniently ignoring the issue of money coming into you.

Wallets in the Information Age

As we move into the Information Resource Economy—Web 3.0—, the role of what we now call a “wallet” will change. For instance, you’re on a website and watch an ad, maybe even click on it. Today, you receive nothing for your attention and engagement (unless you’re using Brave), not to mention your information (ie. personal data) which led to you seeing that ad. Facebook, Google, Twitter, etc receive that money.

But in an information-based economy, you will be paid directly, in real time no less, for providing your information (if you opt in), your attention (for watching the ad), and your engagement (if there’s something asked of you). In this new Internet (3.0 or decentralized), your time on the Internet and social media will involve value flowing into your so-called wallet as you’re paid for your information, attention, and engagement — rather than it flowing to the Facebooks of the world. And, yes, value will flow out, too, as you pay for certain goods and services. But the important thing to note here is that value flows every which way, in and out, more or less seamlessly (thanks to smart contracts).

In this new economy, what we’re calling your wallet will no longer be a standalone application. That would defeat the whole point of an information-based decentralized economy in which value is being produced and shared all the time from every direction — bottom up (for your data), top down (e.g., government benefits), and side to side (peer to peer). The way you store and manage your cryptocurrency will be integrated with all your applications, with all your online activity.

Enter the Anatha Nexus

The Anatha app is, in fact, a nexus of applications — including what people call a crypto wallet. Anatha has a wallet; it is not a wallet per se. Yes, the Anatha Nexus has all the functionality of today’s crypto wallets with some more robust features such as human readable addresses (@name — without any cumbersome extensions—to receive any tokens the wallet supports, pushing cumbersome token addresses to the background), multiple profiles in one app, and customized reporting of your transactions (an increasing demand from the IRS).

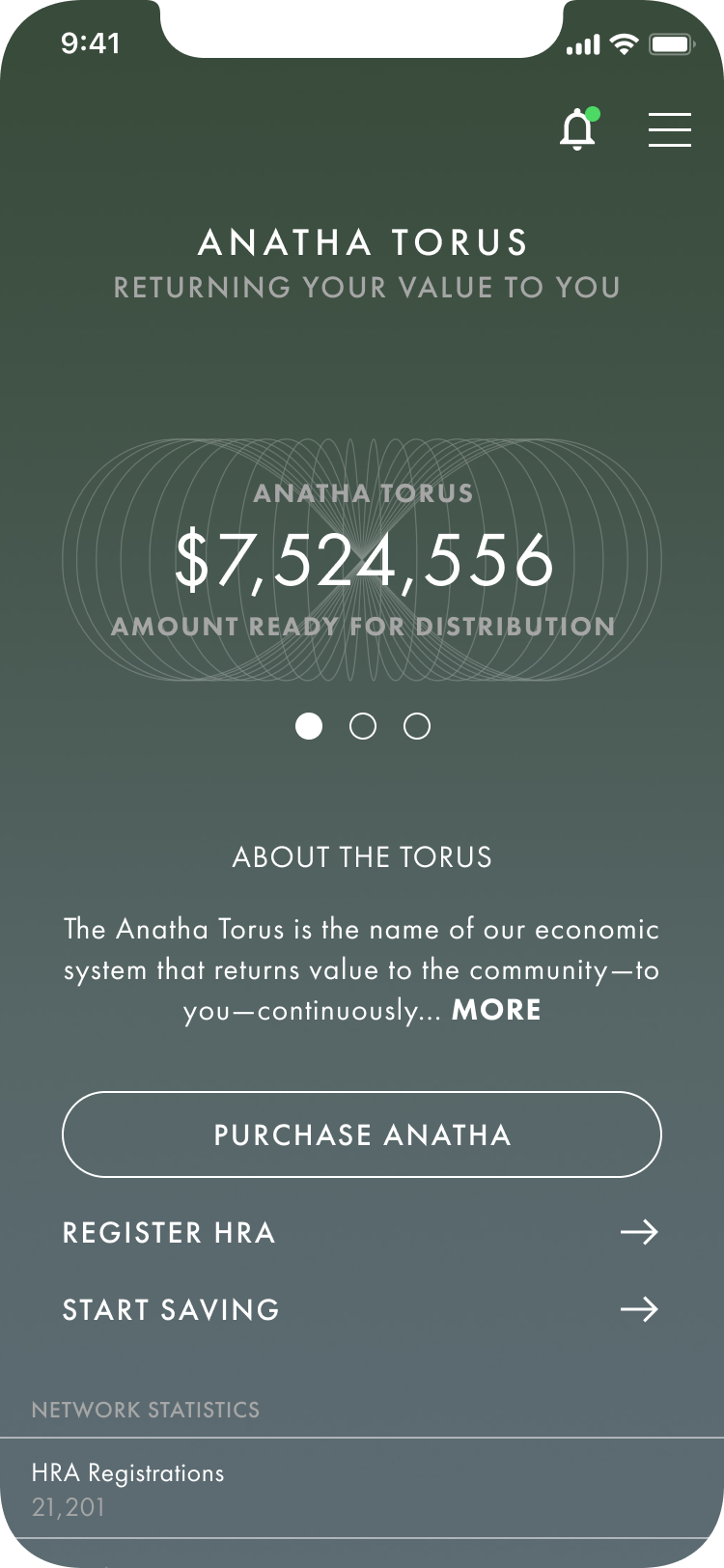

But what makes the Anatha wallet different is that it sits on the Anatha Network (its blockchain built on Cosmos/Tendermint) with its native rewards token, ANATHA. This is not just a way to manage your tokens — although it’s also that; it’s a way to interact with the decentralized world and receive value into your wallet. Most notably, the economics of the network are such that value created on the Anatha Network is distributed to all participants (all holders of an HRA). We call this the Anatha Torus. It’s our mission written directly into code — our belief that value should be shared by those who create it rather than extracted and hoarded by a few.

The Anatha Torus is a mechanism that distributes value daily to HRA holders in the form of our native rewards token. As new functionality is introduced, such as messaging and social content sharing, value will flow faster in all directions — to and from your wallet, to and from other participants.

We started with wallet functionality because we believe that people need to trust you with finances before they trust you with, say, social messaging. WeChat did the opposite: it started as a social application and, over time, integrated financial services. At Anatha, we are going in the reverse direction: starting with financial services and layering in social afterwards to create a thriving economy in which all participants prosper.

What people call a wallet today is going to change dramatically as we enter Web 3.0. It will no longer be a standalone application, an island amid the rivers of value. It will be a layer within all applications — an always-on, multi-directional inflection point within the very creation, distribution, and flow of value itself.

DANIEL COFFEEN

Chief Communications Officer